Frequently Asked Questions that we’ve received so far….

Following the August 2022 passing of the Inflation Reduction Act, which included numerous tax benefits for clean energy installation, we have received some excellent questions from our followers.

While the guidance for these rules is still taking shape, there are some questions that we’re able to address. You can find those below.

Please feel free to submit additional questions to us and stay tuned as we plan to host more events as additional rules and guidance becomes available.

If you’re just getting started, check out the recorded version of our most recent webinar that overviews all of the solar energy tax benefits in the IRA and what we know so far.

We can conduct a quick remote analysis to help. Additional site information is required for project development but an initial look can help take the next step in determining feasibility. Click here if you’re ready to talk with a Solar Consultant.

This is a frequent question, and the answer isn’t always black and white. In short, if the technology available today will meet your goals and the funding is available, then there is little benefit to waiting. Solar is modular and can grow as the technology improves.

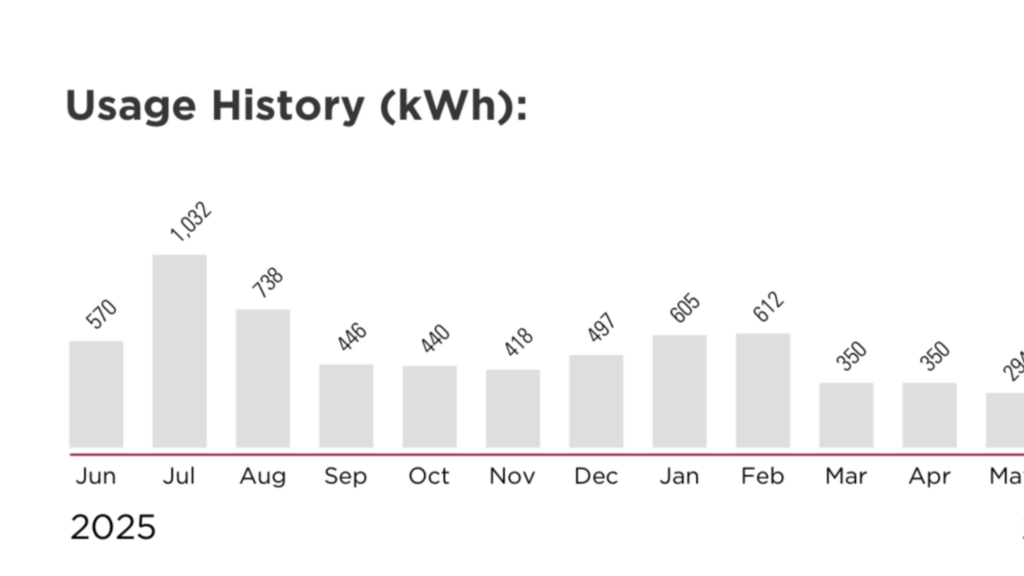

The short answer is yes, though solar is typically designed to offset all of the loads served by your main electrical panel.

Companies (for example, developers) may choose to transfer the ITC or PTC to another taxpayer. Taxpayers who are not tax-exempt entities will be allowed a one-time transfer of these tax credits. Any payments received in exchange for the transfer of credits would be excluded from income, and any amounts paid to obtain a transferred credit could not be deducted from income. Credits that could be transferred would also be given extended carryback and carryforward periods. The carryback period for these credits would be extended from 1 to 3 years, and the carryforward period extended from 20 to 22 years.

The domestic content standard will be set by Treasury under 661 of Federal Regulations. These requirements are 100% steel/iron under 661.5(B) and for manufactured products a 40% requirement through 2024 followed by 45% in 2025, 50% in 2026, and 55% in 2027 and beyond. Manufactured content is further explained: The products which are components of a qualified facility upon completion will be deemed to have been produced in the United States if the adjusted percentage of the total costs of all such manufactured products of the facility are attributable to manufactured products (including components) which are mined, produced, or manufactured in the United States. This section is expected to have further clarification.

It’s always possible that something may surface, though our focus here has been on the Federal bill. A more likely outcome for Ohio will be at the local level.

10%: the project is located in a low-income community 1 or on Indian land. 2 20%: the project is part of a qualified low-income residential building project 3 or a qualified low-income economic benefit project. 4 If the latter, (20% adder) then yes the tenants would need to be renters to qualify. The project must be installed on a residential rental building that is part of a housing program under the Violence Against Women Act, Title V of the Housing Act of 1949, a tribally designated housing entity, or other programs determined by HUD; and the “financial benefits” of the electricity produced by the project are “allocated equitably” among the occupants of the building. See IRA § 13103(a), to be codified at 26 U.S.C. § 48(e)(2)(B).

SEC. 60103. GREENHOUSE GAS REDUCTION FUND. 2 The Clean Air Act is amended by inserting after section 133 of such Act, as added by section 60102 of this Act, 4 the following: 5 ‘‘SEC. 134. GREENHOUSE GAS REDUCTION FUND.

Yes, an S-Corp business can benefit for the available tax credits.

These credits are “Allocated” meaning a company will have to apply to the Treasury to get these particular credits. Treasury can allocate 1.8 GW direct current capacity total of wind and solar credits per year starting for 2023. The project must be installed on a residential rental building that is part of a housing program (including HUD programs) and the “financial benefits” of the electricity produced by the project are “allocated equitably” among the occupants of the building. See IRA § 13103(a), to be codified at 26 U.S.C. § 48(e)(2)(B).

Solar continues to be a great fit for these governmental entities, and traditional funding options such as third party owned systems or Power Purchase Agreements (PPA) continue. A new option included in the IRA allows for these entities to purchase solar outright and benefit from a “direct pay” provision. The criterion for the payment is still being developed, though a government entity may receive a payment equal to what a tax–paying entity would receive. Still, it is tied to the domestic content requirements. We can help you evaluate the option that works best for you.

We are familiar with the code and related documents and can point you and your tax advisors in the right direction to address specific questions. Additionally, our decades of experience in the solar industry have helped us build a network of professionals that work in this space who are better suited to advise on tax specific implications, though we still recommend consulting with your tax professional.

The new Base ITC for projects installed this year is 30%.

Brownfield sites as defined under Sections 101(39)(A), (B), and (D)(ii)(III) of CERCLA; As determined by the Secretary, (1) a metropolitan or non-metropolitan statistical area with unemployment rates, from the previous year, at or above the national average and (2) at least 0.17% of employment or 25% of local tax revenues are related to the extraction, processing, transport, or storage of coal, oil, or natural gas at any time beginning in 2010 Census tracts, plus their adjacent census tracts, where a coal mine closed after 1999 or a coal-fired power plant was retired after 2009.